Smart Investing for Beginners: Little Money, Index Funds, Roth vs Traditional IRA, Passive Income & Long vs Short-Term Planning

Getting Started: Investing with Little Money

Welcome to the exciting journey of building your financial future! 🚀 Many people mistakenly believe that you need a massive inheritance to start, but smart investing for beginners actually starts with just a little money. Whether you are using a modern micro-investing app or a standard brokerage account, the absolute key is the magic of compounding, which turns tiny seeds into massive forests over time. 🌳 Do not wait for a ‘perfect’ moment to enter the market because time in the market consistently beats trying to time the market. 📉 Even investing as little as $50 a month can lead to significant wealth if you remain consistent and disciplined. Why should you start right now? Here are a few compelling reasons:

- Compound interest works best over decades, not just a few days.

- Starting small lowers the psychological barrier to entry for most people.

- You can learn market mechanics without risking your entire life savings at once.

It is all about shifting your mindset from being a consumer to becoming an owner. 💸 Every single dollar you invest is like a little soldier working tirelessly for your future self while you sleep. By prioritizing your future today, you are creating a safety net that will eventually provide total financial freedom. Just remember that the best time to plant a tree was twenty years ago, but the second best time is today. The journey of a thousand miles begins with a single, small contribution to your portfolio. Small steps today lead to big leaps tomorrow! You have the power to change your financial destiny starting right now.

The Power of Index Funds and Passive Income

Once you have decided to start your journey, the next big question is what to actually buy, and that is where Index Funds come into play as the ultimate beginner tool. 📊 Instead of trying to find the next ‘unicorn’ stock or a risky gamble, index funds allow you to own a tiny piece of the entire market. For instance, an S&P 500 index fund tracks the performance of the 500 largest companies in the United States. 🇺🇸 This instant diversification significantly reduces your risk because even if one company fails, the hundreds of others keep the economic engine moving forward. 🚂 Index funds are also the backbone of a reliable passive income strategy because many of these companies pay dividends. 🔄 You can choose to have these dividends automatically reinvested to buy even more shares, accelerating your growth without extra effort. Here is why index funds are often the best choice:

- They have extremely low fees compared to actively managed mutual funds.

- They provide instant diversification across sectors like technology and healthcare.

- There is zero need for constant market monitoring or expert financial knowledge.

By keeping your expenses low and your diversification high, you are essentially ‘winning by not losing.’ 🏆 It is a simple, effective, and stress-free way to build wealth without needing a finance degree. You don’t need to be a Wall Street pro to get professional results. Simply put, buying the whole haystack is much smarter than searching for a needle. This approach allows you to benefit from the overall growth of the global economy. Building wealth is about consistency, not complexity.

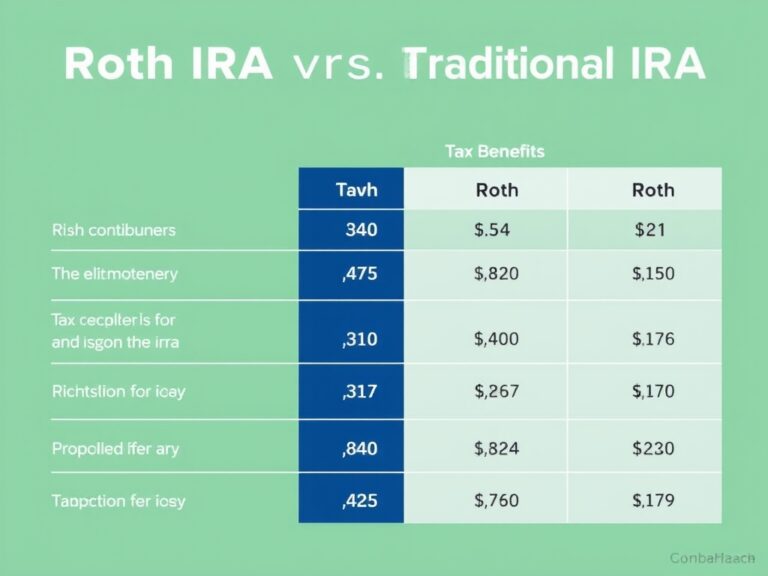

Roth vs Traditional IRA: Winning the Tax Game

Now, let’s dive into where you should put those investments to save on taxes, specifically focusing on the Roth vs Traditional IRA debate. 🏦 A Traditional IRA gives you a tax break today by letting you deduct your contributions from your taxable income, but you will pay taxes when you withdraw later. 👴 Conversely, a Roth IRA uses after-tax dollars now, but your future withdrawals—including all those juicy gains—are completely tax-free! 🎁 Deciding between these two accounts usually depends on whether you think your tax bracket will be higher now or when you reach retirement age. ⚖️ Most beginners gravitate toward the Roth IRA because of its long-term tax advantages and the peace of mind it offers. 🛡️ Consider these primary differences before you open an account:

- Traditional: Best if you are currently in a high tax bracket and want immediate savings.

- Roth: Best for young investors who expect their future income to grow significantly.

- Withdrawals: Roth IRAs offer more flexibility, allowing you to withdraw contributions at any time.

Choosing the right tax-advantaged bucket for your money can save you hundreds of thousands of dollars over your lifetime. 💰 It is one of the most powerful ‘hacks’ available in the modern financial world. Make sure to check the current annual contribution limits so you do not miss out on these opportunities. Don’t let the complexity of tax law prevent you from starting your retirement account today. Taxes can be your biggest expense in retirement, so planning ahead is vital. Your future self will certainly thank you for being tax-savvy right from the start. Every dollar saved in taxes is a dollar that stays in your pocket. Take the time to evaluate your options and choose the path that fits your goals.

Long-Term vs Short-Term Planning: Your Roadmap

Finally, successful investing requires a clear distinction between Long-Term vs Short-Term Planning to ensure your strategy aligns with your personal life goals. 🗺️ Short-term goals, such as buying a house or a new car within the next two years, should typically stay in ‘safe’ spots. 🏠 You might consider high-yield savings accounts or Certificates of Deposit (CDs) for these funds to avoid the natural volatility of the stock market. On the other hand, long-term planning for retirement allows you to weather the inevitable storms of the market because you have decades to recover. 🌊 It’s crucial to understand your own risk tolerance before you start putting your hard-earned cash into volatile assets. 🎢 A smart investor stays the course during a market downturn, viewing it as a ‘sale’ on great companies rather than a reason to panic. 🛒 Balancing these two timelines is the secret sauce to maintaining a stress-free and productive financial life. 🍲 Consider these steps for a balanced and robust approach:

- Build an emergency fund first to cover three to six months of living expenses.

- Automate your monthly investments so you are never tempted to skip a contribution.

- Rebalance your portfolio annually to keep your risk levels in line with your goals.

By having a clear roadmap, you stop reacting emotionally to the daily news cycle and start acting strategically. 🎯 Your journey to wealth is definitely not a sprint; it is a marathon where the most patient and consistent person wins. Discipline and patience are the most valuable assets any investor can ever own. Financial freedom is not about how much you make, but how much you keep and grow. Take the first step today and watch your future transform! Your future is unwritten, and you have the pen.