Investing for Beginners: Low-Cost Strategies, Index Funds, IRA Choices, and Passive Income for Long-Term Wealth

Welcome to the world of building long-term wealth! Starting your journey in investing for beginners might feel like learning a new language, but it’s actually the most empowering step you can take for your future self. Think of investing not as a way to get rich quick, but as a reliable vehicle to outpace inflation and secure your financial freedom. 🚀 Most people hesitate because they fear losing money, yet the biggest risk is often doing nothing at all while your savings lose purchasing power. By understanding basic market principles, you can transform from a consumer into an owner of global businesses. 📈 This post will guide you through the essentials of low-cost strategies and smart IRA choices that minimize fees and maximize growth. We’ll dive into how index funds act as the backbone of a solid portfolio, providing diversification without the stress of picking individual stocks. Whether you’re 22 or 42, the best time to start was yesterday, and the second best time is right now. Let’s break down the complexities into actionable steps so you can start generating passive income today. Remember, the goal is consistency over intensity; small, regular contributions are the secret sauce to a multi-million dollar nest egg. Are you ready to take control of your financial destiny? Let’s get started with the basics of smart, low-cost investing.

Mastering Low-Cost Strategies and Index Funds

When you’re just starting, the most important rule is to keep your costs as low as possible because every dollar paid in fees is a dollar that isn’t compounding for you. This is why index funds have become the gold standard for savvy beginners; they allow you to own a piece of hundreds of companies at once for a tiny fraction of the cost of actively managed funds. 🏦 Expense ratios are the silent killers of wealth, so looking for funds with fees below 0.10% is a critical move for your long-term success. Instead of trying to find the next hot stock, you are simply buying the entire market, which historically has returned about 7-10% annually. 📊 Here is why index funds are a game-changer:

- Instant Diversification: You reduce the risk of a single company failing ruining your portfolio.

- Low Maintenance: No need to spend hours analyzing balance sheets or watching news cycles.

- Tax Efficiency: These funds generally trade less frequently, meaning fewer capital gains taxes for you.

By sticking to a passive investing approach, you avoid the emotional pitfalls of market timing and the high costs of expert advisors who rarely beat the market anyway. It’s about being average in the best way possible—capturing the total growth of the economy without the stress. 🐢 Slow and steady truly wins the race when you utilize these low-cost vehicles. Investing should be boring, like watching paint dry or grass grow, because that’s how real wealth is built over decades. Focus on the long game, ignore the daily market noise, and let the low-cost strategies do the heavy lifting for you.

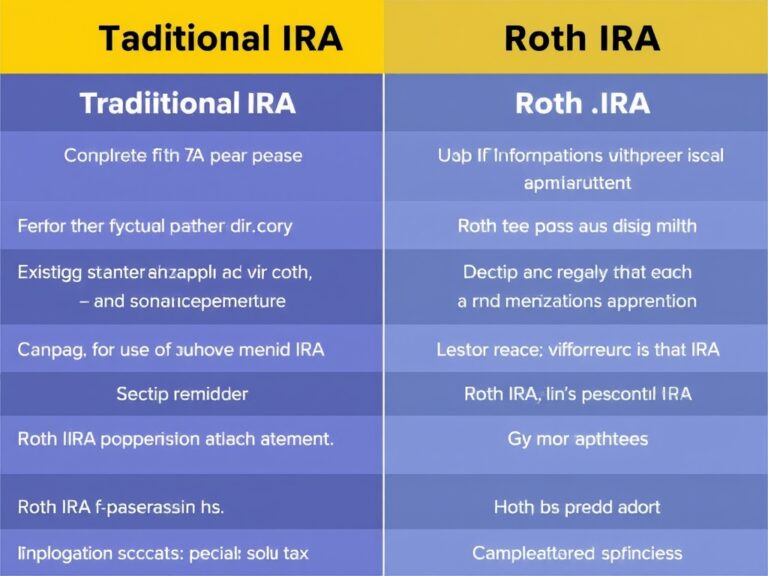

Choosing the Right Retirement Vessel: IRA Choices Explained

Once you’ve selected your low-cost index funds, you need to decide where to park them, and this is where your IRA choices come into play. Individual Retirement Accounts (IRAs) offer incredible tax advantages that can save you six figures in taxes over your lifetime. 🛡️ The two main heavyweights are the Traditional IRA and the Roth IRA, and choosing between them depends on your current tax bracket versus your expected future bracket. In a Traditional IRA, your contributions may be tax-deductible today, but you’ll pay income tax on withdrawals during retirement. Conversely, the Roth IRA is a crowd favorite for beginners because you contribute after-tax money, meaning your investments grow tax-free and your withdrawals in retirement are also tax-free. 🌟 Imagine having a million dollars in an account and being able to spend every single cent without giving the IRS a cut!

- Traditional IRA: Best if you are currently in a high tax bracket and want a tax break now.

- Roth IRA: Ideal for younger investors who expect to be in a higher tax bracket later in life.

- Contribution Limits: Be aware of the annual caps set by the IRS to maximize your benefits.

Understanding these nuances is key to long-term wealth preservation and strategic financial planning. Don’t let the paperwork intimidate you; most major brokerages make opening an account as easy as ordering a pizza. By automating your contributions to these accounts, you ensure that you are paying yourself first before you can spend that money elsewhere. This disciplined approach to tax-advantaged investing is the foundation of a rock-solid financial plan.

Generating Passive Income and the Magic of Compounding

The ultimate dream of every investor is to create a stream of passive income that covers their living expenses without having to work a traditional job. This is achieved through the dual power of dividend-paying stocks and the incredible phenomenon known as compound interest. 🧪 Albert Einstein famously called compound interest the eighth wonder of the world because of its ability to turn modest sums into fortunes over time. When you reinvest your dividends—the payments companies give you just for owning their stock—you are buying more shares, which in turn generate even more dividends. 🔄 This virtuous cycle accelerates your wealth-building journey, especially when you start early and stay consistent. To maximize this, you should look for Dividend Aristocrats, which are companies that have increased their dividends for at least 25 consecutive years.

- DRIP (Dividend Reinvestment Plan): Automatically uses your dividends to buy more shares.

- Time Horizon: The longer your money stays in the market, the more heavy lifting compounding does.

- Yield: Look for a healthy balance between current income and future growth.

By focusing on long-term wealth rather than short-term gains, you allow the math to work in your favor. Even small amounts, like $100 a month, can grow into a substantial sum if given enough time and a consistent reinvestment strategy. Think of your portfolio as a money tree that you are planting today; in the beginning, it needs care and regular watering, but eventually, it will provide shade and fruit for the rest of your life. 🌳 This is the essence of financial independence: making your money work harder for you than you ever worked for it.

Portfolio Diversification and Staying the Course

To protect your hard-earned capital, you must embrace portfolio diversification and effective risk management. While index funds provide a great start, a truly robust strategy might include a mix of domestic stocks, international equities, and perhaps some bonds for stability. 🌍 Diversification ensures that when one sector of the economy is struggling, other areas of your portfolio can help pick up the slack. ⚖️ It’s also vital to understand your own risk tolerance; can you handle a 20% market dip without panicking and selling? Successful investing for beginners isn’t just about math; it’s about psychology and having the discipline to stay the course during market volatility. Emotional decisions are often the most expensive mistakes an investor can make, so having a written plan helps you stay rational when the headlines get scary.

- Asset Allocation: The specific mix of stocks, bonds, and cash based on your age and goals.

- Rebalancing: Periodically adjusting your portfolio to maintain your desired risk level.

- Emergency Fund: Always keep cash on hand so you never have to sell investments at a loss.

As you build your long-term wealth, remember that the market goes up more often than it goes down, but the down periods are a natural part of the cycle. By staying invested through the dips, you position yourself to capture the inevitable recoveries that follow. 🧗♂️ Education is your best defense against fear, so keep learning about market history and the fundamentals of the companies you own. You are now equipped with the knowledge to start your passive income journey with confidence and clarity. The road to wealth is a marathon, not a sprint, and you’ve already taken the most important first step by educating yourself today. 🏁