How to Start Investing with Little Money: Best Index Funds, Roth vs Traditional IRA, Passive Income, and Long-Term vs Short-Term Strategies

Building the Wealth Mindset from Scratch

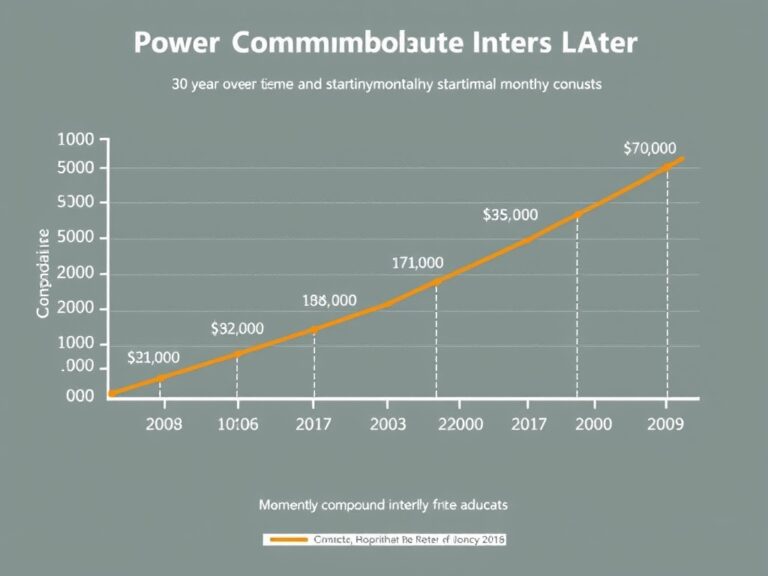

Hey there! Are you sitting around thinking you need a massive windfall to start your investment journey? 💰 Well, I’ve got some great news: starting small is actually one of the smartest ways to build wealth. Many people believe that investing is only for the wealthy elite, but that couldn’t be further from the truth in today’s digital age. With fractional shares and no-commission apps, you can literally start with the price of a single latte. The most critical factor isn’t how much you start with, but when you start, because time is your greatest ally. ⏳ By putting even $20 or $50 a month into the market, you trigger the ‘eighth wonder of the world’—compound interest. This means your money earns interest, and then that interest earns interest, creating a snowball effect. Don’t wait for the ‘perfect’ moment or a high-paying promotion to get in the game. You should focus on building the habit of consistency rather than focusing on the initial dollar amount. Every dollar you invest today is a seed for your future financial freedom. Let’s dive into how you can make this happen without breaking the bank!

The Power of Best Index Funds

Now, let’s talk about the Best Index Funds, which are the absolute gold standard for beginners with limited capital. 📈 Instead of trying to pick the ‘next big stock’ like a gambler, index funds allow you to own a tiny piece of hundreds or thousands of companies simultaneously. This instant diversification significantly lowers your risk because if one company fails, the others are there to balance the scale. Low-cost funds like the Vanguard Total Stock Market ETF (VTI) or the S&P 500 ETF (VOO) are perfect choices for long-term growth. They come with incredibly low expense ratios, meaning you keep more of your hard-earned money instead of giving it away in fees. 🏦 Many of these funds track the overall market performance, which has historically averaged about 7-10% annually. Here are a few reasons why index funds win:

- Low Maintenance: You don’t need to spend hours researching individual stocks.

- Diversification: Spreads your risk across various sectors like tech, healthcare, and finance.

- Low Cost: Fees are often less than 0.05%.

By choosing these broad-market funds, you’re essentially betting on the long-term success of the entire economy. It’s a ‘set it and forget it’ strategy that outperforms most professional hedge fund managers over time. Start by looking for ‘No-Transaction-Fee’ funds on your brokerage platform to maximize your small initial deposits. This approach minimizes the impact of market noise and keeps you focused on your wealth-building goals.

Roth vs. Traditional IRA: The Tax Battle

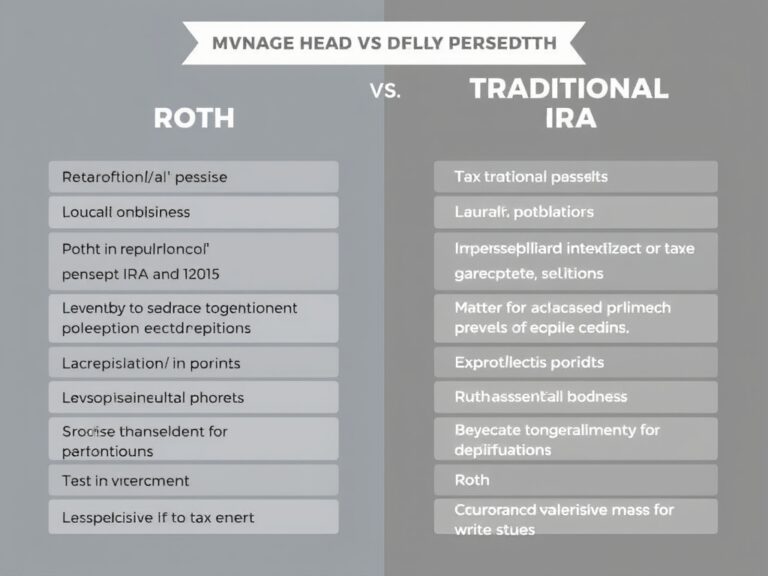

One of the most important decisions you’ll make is choosing between a Roth IRA and a Traditional IRA. 🏦 Understanding these accounts is vital because they determine how the government taxes your retirement savings. A Roth IRA is often a favorite for young investors because you contribute money that has already been taxed, meaning your withdrawals in retirement are 100% tax-free! 💸 On the other hand, a Traditional IRA allows you to deduct your contributions from your current income, lowering your tax bill today, but you’ll have to pay taxes when you take the money out later. If you expect to be in a higher tax bracket when you retire, the Roth is usually the superior choice. However, if you need the tax break right now to free up more cash for investing, the Traditional might be the way to go. Here is a quick comparison of the two:

- Roth IRA: Post-tax contributions, tax-free growth, tax-free withdrawals.

- Traditional IRA: Pre-tax contributions, tax-deferred growth, taxed withdrawals.

Both accounts have annual contribution limits, so try to hit those if you can, but even small contributions are better than none. Choosing the right ‘bucket’ for your investments can save you tens of thousands of dollars in the long run. Always consider your current income level versus your future goals when making this choice. Investing in an IRA is one of the most efficient ways to use your dollars for long-term growth.

Creating Your Passive Income Snowball

Let’s explore the exciting world of Passive Income and how it can accelerate your journey to financial independence. 🌊 Passive income is essentially money that works for you while you sleep, and in the stock market, this usually comes in the form of dividends. Dividends are portions of a company’s profit paid out to shareholders, and when you’re starting with little money, reinvesting these is crucial. 💎 By using a Dividend Reinvestment Plan (DRIP), your brokerage automatically buys more shares with your dividend payouts, increasing your ownership without you lifting a finger. Over time, these small payments grow into a substantial stream of cash flow that can eventually cover your living expenses. Beyond dividends, you might look into Real Estate Investment Trusts (REITs), which allow you to invest in property portfolios with just a few dollars. The goal is to create a self-sustaining cycle where your assets generate enough profit to buy more assets. 🔄 It’s like planting a fruit tree; at first, it requires care, but eventually, it provides fruit every season with minimal effort. Building this stream takes patience, but the psychological boost of seeing money hit your account is incredibly motivating. Remember, every share you buy is a tiny ’employee’ working 24/7 to earn you more money. This constant cash flow reduces your reliance on a traditional paycheck and builds real freedom.

Long-Term vs. Short-Term Strategies

Finally, we need to distinguish between Long-Term vs. Short-Term Strategies to ensure you stay on the right path. ⚖️ Short-term trading or ‘day trading’ is often what people see on social media, but it is extremely risky and often leads to losses for beginners with limited funds. Long-term investing, however, focuses on holding assets for years or even decades, allowing you to ride out the inevitable market volatility. 🎢 When the market dips, long-term investors see it as a ‘sale’ rather than a disaster. You should only invest money that you don’t need for the next five years to avoid being forced to sell during a market downturn. Short-term goals, like a vacation or a house down payment, should usually stay in high-yield savings accounts or low-risk bonds instead of the stock market. 🏦 By keeping your ’emergency fund’ separate, you protect your long-term investments from being liquidated at the wrong time. Here’s a simple breakdown of the mindset difference between these approaches:

- Short-Term Strategy: High stress, high risk, focus on ‘timing’ the market.

- Long-Term Strategy: Low stress, historical growth, focus on ‘time in’ the market.

Successful investors understand that wealth is built over decades, not days. Focus on the horizon, stay disciplined during the dips, and your future self will thank you for the patience you showed today. By committing to a long-term plan, you transform from a speculator into a true builder of wealth.