Beginner’s Guide: Start Investing with Little Money, Best Index Funds, IRA Options, Passive Income & Long-Term Strategies

🚀 Kickstarting Your Financial Journey on a Shoestring Budget

Many people believe that the stock market is a playground reserved exclusively for the wealthy, but I’m here to tell you that starting small is the smartest move you can make today. You don’t need a massive windfall to begin; in fact, thanks to modern technology and fractional shares, you can start investing with as little as $5 or even just your spare change. The key is to shift your mindset from ‘I don’t have enough’ to ‘I am building a foundation,’ because even tiny contributions grow significantly over time. When you use micro-investing platforms, you are effectively buying small pieces of massive companies that would otherwise be unaffordable.

- Start by setting aside a small percentage of your paycheck automatically.

- Look into apps that offer fractional share trading to maximize every dollar.

- Focus on consistency rather than the total amount invested each month.

By removing the barrier of entry, you allow compound interest to start working its magic earlier in your life. Remember, the best time to plant a tree was twenty years ago, but the second-best time is right now. Don’t wait for the ‘perfect’ financial moment because it rarely arrives without a proactive start. Every dollar you invest today is a seed for your future financial freedom and independence. By embracing this approach, you are already ahead of the majority of people who are still sitting on the sidelines. You are no longer just a consumer; you are becoming an owner of the global economy. This shift in perspective is the first and most important step toward true financial security.

📈 The Magic of Index Funds: Why They’re the Gold Standard for Beginners

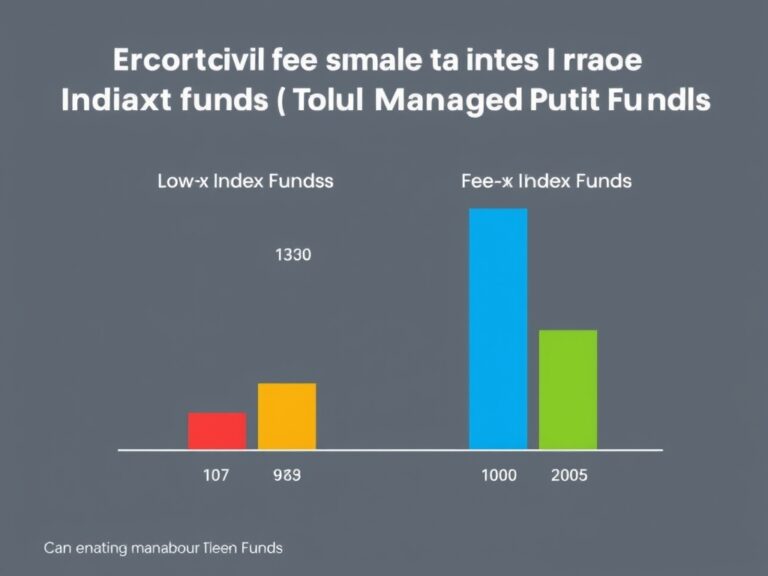

If you’re feeling overwhelmed by the thousands of individual stocks available, index funds are going to be your new best friend for long-term growth. Instead of trying to find the next ‘unicorn’ company, an index fund allows you to buy a basket of stocks that represent a specific sector or the entire market. For instance, an S&P 500 index fund gives you a piece of the 500 largest companies in the U.S., providing instant diversification and lowering your overall risk.

- Low Fees: Most index funds have very low expense ratios compared to actively managed funds.

- Diversification: You aren’t putting all your eggs in one basket, which protects your capital.

- Proven Returns: Historically, index funds outperform the majority of professional stock pickers over time.

It is much easier to ride the wave of the entire economy than to guess which individual company will win or lose. Names like Vanguard (VOO) or Fidelity (FXAIX) are staples in many beginner portfolios because they are efficient and incredibly cost-effective. You won’t have to spend hours analyzing balance sheets; instead, you simply trust the upward trajectory of the broader market. This ‘hands-off’ approach is perfect for beginners who want to build wealth without the stress of daily trading. Index funds provide a solid anchor for any portfolio, ensuring you participate in the growth of industry giants. They offer a simple, low-maintenance way to build wealth over several decades. Even legendary investors like Warren Buffett recommend them for the average person starting out. By choosing index funds, you are betting on the collective success of hundreds of businesses rather than just one.

🏦 Maximizing Growth with IRAs: Choosing Between Roth and Traditional

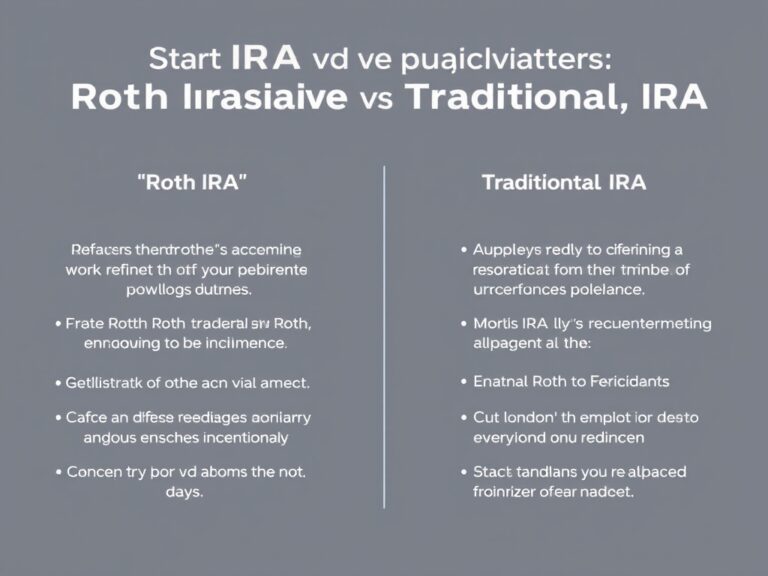

Once you’ve decided what to invest in, you need to decide where to hold those investments, and an Individual Retirement Account (IRA) is often the best choice for tax efficiency. There are two main flavors to consider: the Roth IRA and the Traditional IRA, each offering unique benefits depending on your current income. In a Roth IRA, you contribute after-tax money, meaning your withdrawals in retirement are completely tax-free—a massive win if you expect to be in a higher tax bracket later. Conversely, a Traditional IRA may offer an immediate tax deduction on your contributions today, which can help lower your taxable income right now.

- Choose a Roth IRA if you want tax-free growth and are currently in a lower tax bracket.

- Consider a Traditional IRA if you need a tax break this year and expect lower income in retirement.

- Always be aware of annual contribution limits set by the IRS to stay compliant.

Understanding these nuances helps you keep more of your hard-earned money instead of handing it over to the government. Think of an IRA as a protective shield for your investments, allowing them to compound without the ‘drag’ of annual taxes. It’s one of the most powerful tools available to the average investor for building a multi-generational legacy. Don’t overlook the power of these accounts just because they are labeled for ‘retirement’; they are essential for anyone serious about long-term wealth. Setting one up is usually as simple as opening a brokerage account and selecting the IRA option at a major financial institution. Many beginners find the Roth IRA particularly appealing because of the flexibility it offers with contribution withdrawals. It creates a tax-free bucket of wealth that can provide immense peace of mind in your later years. Deciding on the right vehicle early on sets the stage for maximum efficiency as your portfolio grows.

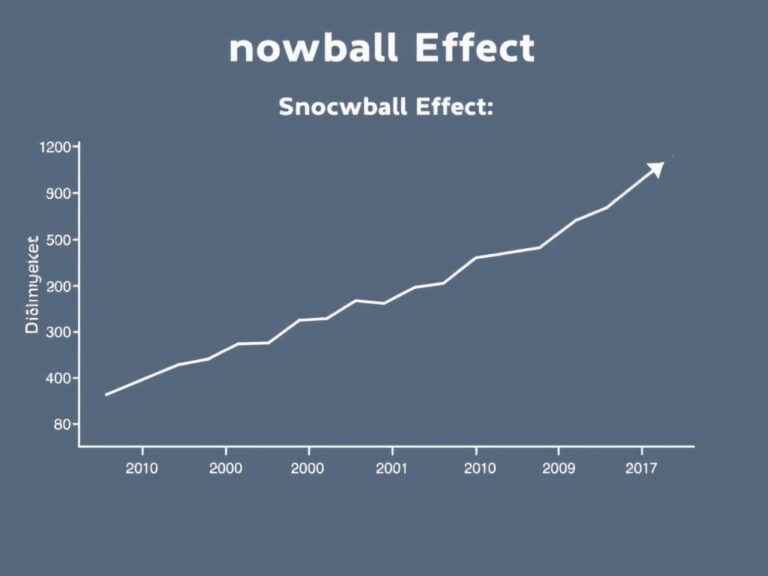

🧘 The Long Game: Cultivating Passive Income and Staying the Course

The final piece of the puzzle is developing a long-term strategy that prioritizes consistency and ignores the ‘noise’ of the daily news cycle. True wealth isn’t built overnight; it is the result of years of disciplined habits and reinvesting your earnings to create passive income. One of the best ways to do this is through a Dividend Reinvestment Plan (DRIP), which automatically uses your dividends to buy more shares of your funds. Over time, this creates a snowball effect where you own more and more shares, which in turn pay more dividends, accelerating your growth exponentially.

- Dollar-Cost Averaging: Invest a fixed amount regularly, regardless of market price, to lower your average cost per share.

- Emotional Discipline: Avoid the urge to sell when the market dips; these are often the best times to buy more.

- Reinvest Everything: Keeping your gains in the market is the fastest way to reach your financial goals.

Passive income is the ultimate goal because it allows your money to work for you while you sleep, eventually covering your living expenses. Stay focused on your ‘why’—whether it’s early retirement, buying a home, or providing for your family—and let time be your greatest ally. Market fluctuations are normal and expected, so don’t let a temporary downturn derail your long-term vision. By staying the course and sticking to your plan, you transform from a casual saver into a sophisticated investor. Consistency is the secret sauce that turns small, humble beginnings into a life-changing financial portfolio. If you keep adding to your accounts and stay patient, the results will eventually speak for themselves. This journey is a marathon, not a sprint, and the finish line is a life of financial freedom. Commit to the process today and watch your future self thank you for the foresight.