Beginner’s Guide to Investing with Little Money: Index Funds, IRAs, Passive Income, and Long-Term Strategies

Hey there, future wealth builder! If you’ve ever felt like the stock market is an exclusive club reserved only for the ultra-wealthy, I am here to completely shatter that myth today. You absolutely do not need a mountain of cash to start your wealth-building journey; in fact, learning how to start investing with little money is one of the smartest financial moves you can make. Thanks to modern financial technology, the barriers to entry have completely crumbled, allowing anyone with a smartphone and a spare five dollars to get skin in the game. By starting early, even with micro-amounts, you leverage the unmatched power of compound interest, which acts like a snowball rolling down a hill, multiplying your wealth over time. Imagine putting just $5 a day into an investment account instead of spending it on a daily latte—over thirty years, that small habit can grow into a staggering nest egg. Today, we are going to explore how you can easily kickstart your financial journey using simple, beginner-friendly tools and strategies. We will break down complex concepts like index funds, IRAs, and passive income streams into bite-sized, actionable steps that you can implement immediately. Here is what we will cover in this guide:

- Micro-Investing: How to turn your spare change into a powerful investment portfolio.

- Index Funds & ETFs: The ultimate low-cost, hands-off way to own pieces of hundreds of top companies.

- Tax-Advantaged Accounts: Why using IRAs can supercharge your long-term savings by saving you on taxes.

- Consistent Habits: How dollar-cost averaging keeps you winning regardless of stock market volatility.

Remember, the best time to start investing was ten years ago, but the second best time is right now. You do not have to be an expert mathematician or a Wall Street guru to succeed here. All you need is a willingness to learn and the discipline to stay the course over the long haul.

Now that you understand that starting small is a superpower, let’s discuss the single best investment vehicle for beginners: index funds and ETFs. An index fund is essentially a basket of stocks that automatically tracks a specific market index, like the S&P 500, which represents the 500 largest publicly traded companies in the United States. Instead of putting all your eggs in one basket by buying individual stocks, you are instantly diversifying your money across hundreds of companies with a single purchase. This passive approach means you don’t have to spend hours researching individual balance sheets or trying to predict stock market trends. Over long periods, index funds have consistently outperformed the vast majority of active mutual fund managers, making them an absolute staple of any long-term strategy. Many modern brokerage platforms now allow you to purchase fractional shares, meaning you can buy $10 worth of an index fund even if a single full share costs $400. To maximize your success with index funds, keep these core principles in mind:

- Low Expense Ratios: Look for funds with rock-bottom fees (ideally under 0.10%) so your returns stay in your pocket.

- Broad Diversification: Choose total stock market funds to capture the growth of the entire economy.

- Fractional Shares: Leverage brokerages that let you invest exact dollar amounts regardless of share price.

By keeping your fees low and your diversification high, you build a resilient foundation that quietly grows your wealth. This set-it-and-forget-it approach is perfect for busy people who want their money to work hard while they sleep. It turns the stock market from a high-stress gambling arena into a reliable, wealth-building machine. You can literally start this process today with less than the cost of a single restaurant meal.

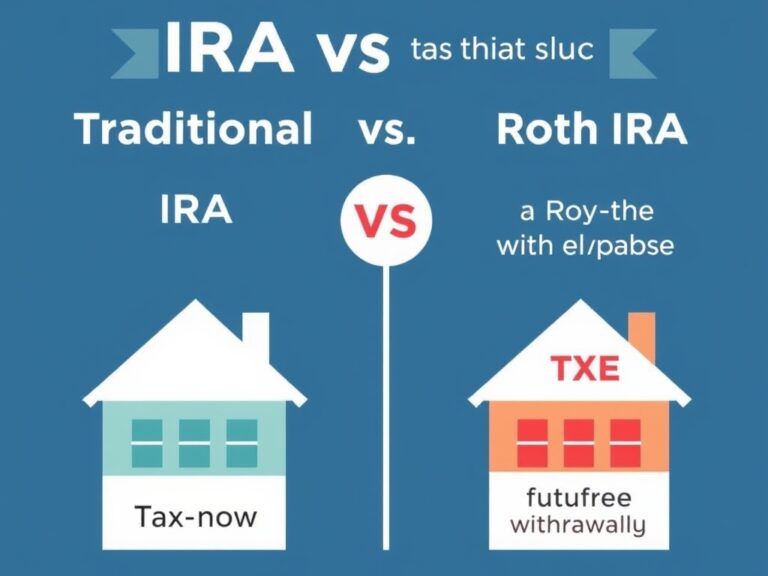

Once you have selected your investments, the next critical step is deciding where to hold them, and that is where IRAs (Individual Retirement Accounts) come in to save the day. IRAs are specialized personal accounts designed specifically to help you build a retirement nest egg while offering massive, government-approved tax advantages. There are two primary types of IRAs you should know about: the Traditional IRA and the Roth IRA, each serving different financial situations. With a Traditional IRA, your contributions are often tax-deductible today, meaning you pay fewer taxes now, but you will pay taxes on your withdrawals when you retire. On the flip side, a Roth IRA is funded with after-tax dollars, meaning you get no immediate tax break, but your money grows entirely tax-free and your future withdrawals are 100% tax-exempt. For beginners who expect to earn more money later in their careers, the Roth IRA is often a fan favorite because tax-free growth is incredibly powerful over several decades. Let’s compare the key benefits of these tax shelters so you can decide which one fits your current goals:

- Traditional IRA: Great for immediate tax relief if you are currently in a high income-tax bracket.

- Roth IRA: Ideal for younger investors because you lock in tax-free withdrawals for your retirement years.

- Automatic Investing: You can set up automatic monthly contributions directly from your checking account.

Utilizing these accounts ensures you aren’t needlessly giving away a large portion of your hard-earned profits to Uncle Sam. By combining the power of index funds with the tax advantages of an IRA, you create a highly efficient compounding machine. Don’t leave free money on the table; opening an IRA is incredibly simple and can be done online in under ten minutes. Taking this small step today sets up a highly secure foundation for your future self.

One of the most exciting milestones on any investor’s journey is watching their money start generating passive income automatically. Passive income is essentially money earned with minimal active effort, allowing you to gradually decouple your time from your earning potential. When you invest in dividend-paying index funds or stock portfolios, companies literally pay you cash rewards just for owning their shares. Instead of spending these dividend payouts, you can set them to automatically reinvest, buying more fractional shares and accelerating your compounding growth. This strategy is known as a Dividend Reinvestment Plan (DRIP), and it is a secret weapon used by wealthy investors to quietly compound portfolios without adding extra capital. Over time, these reinvested dividends create a snowball effect, dramatically increasing the size of your portfolio and future payout amounts. To build a robust passive income engine from scratch, consider focusing on these main pillars:

- Dividend ETFs: Funds specifically curated to hold stable, cash-generating companies that regularly share profits.

- Reinvestment (DRIP): Automatically using cash dividends to buy more shares, completely hands-free.

- Patience and Time: Allowing the cash flow to build up silently over years until it can cover your daily expenses.

Imagine waking up to find that your portfolio earned you enough money overnight to pay your phone bill or buy your groceries. That is the magic of passive income, and it starts with the very first dollar you decide to invest today. By remaining consistent, you eventually build an automated income stream that provides true financial freedom. Every tiny contribution you make today is a building block for a self-sustaining financial future.

To survive and thrive in the stock market, you need robust, battle-tested long-term strategies that shield you from emotional decision-making. The most powerful strategy for beginners investing with little money is called dollar-cost averaging (DCA). With dollar-cost averaging, you invest a fixed amount of money at regular intervals—say, $20 every single week—regardless of whether the market is up, down, or flat. When prices are high, your fixed investment buys fewer shares; when prices drop, your investment automatically buys more shares at a discount. This completely eliminates the stressful, and often losing, game of trying to ‘time the market’ to buy at the perfect absolute bottom. Historically, the stock market has always recovered from temporary downturns and gone on to reach new highs, rewarding patient investors who stayed disciplined. By committing to a long-term horizon of five, ten, or twenty years, you transform temporary market volatility into your greatest ally. Here are the golden rules of a successful long-term investing mindset:

- Consistency Over Timing: Keep investing regularly, because consistency beats trying to predict market movements every time.

- Ignore Short-Term Noise: Turn off the daily financial news and focus entirely on your long-term personal goals.

- Automate Everything: Set up automatic transfers so your investing happens quietly in the background without daily effort.

Your wealth journey is not a 100-meter sprint; it is a long, highly rewarding marathon that values persistence above all else. By implementing these simple, low-cost strategies, you are taking absolute control of your financial destiny, one small dollar at a time. Start small, stay consistent, and watch your financial freedom grow step by step!